Key Takeaways:

A Property Finance Playbook

A Property Finance Playbook is a simple set of rules smart investors follow to set up their loans correctly. It helps them grow their property portfolio and protect their assets.

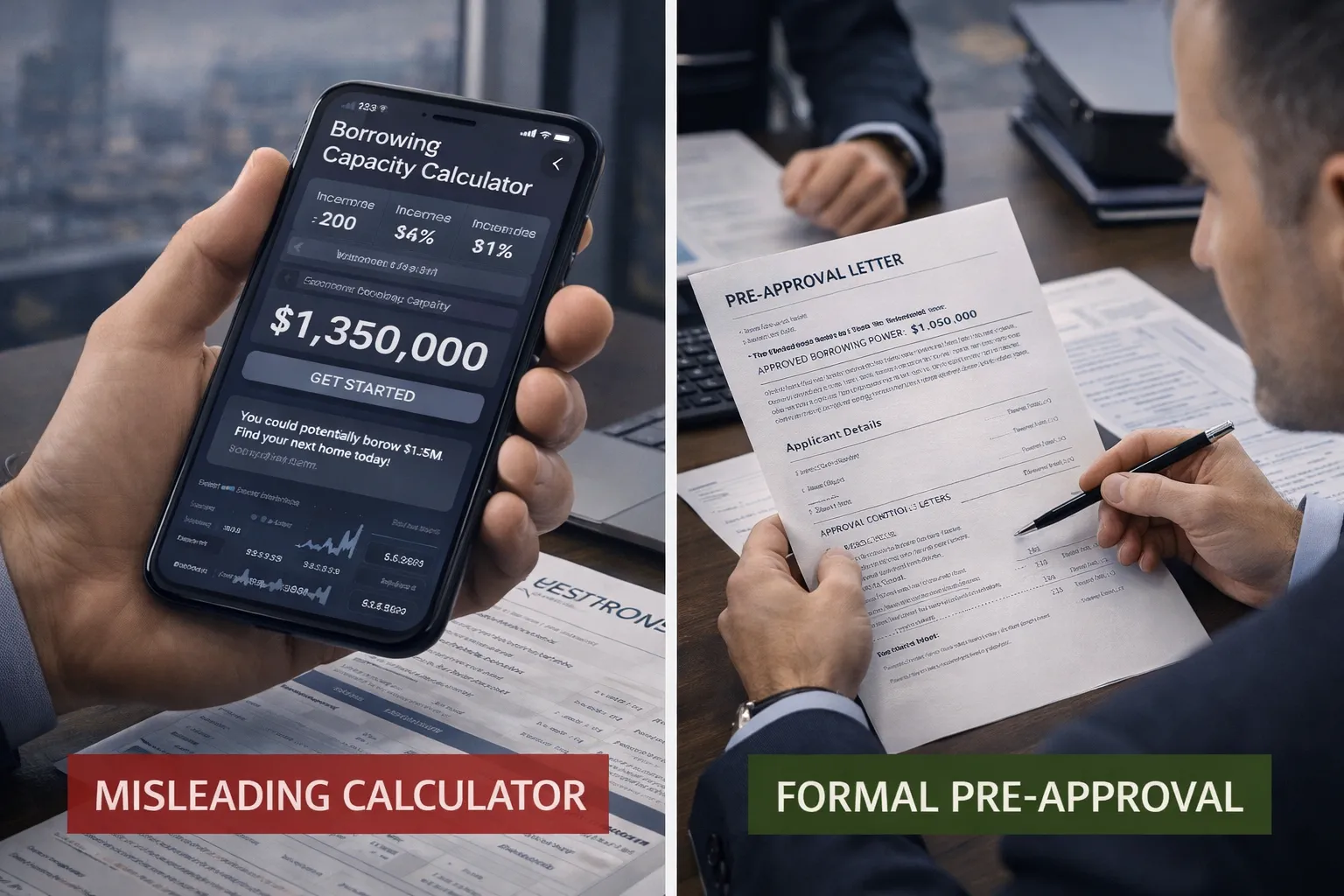

Strategy 1: Get Preapproved for a Mortgage.

A formal preapproval is the only way to know your true borrowing power, as it removes guesswork and prevents you from wasting time.

Strategy 2: Understand Property Value.

An independent valuation report provides objective evidence of a property's worth. This protects you from overpaying and the costs of Lender's Mortgage Insurance.

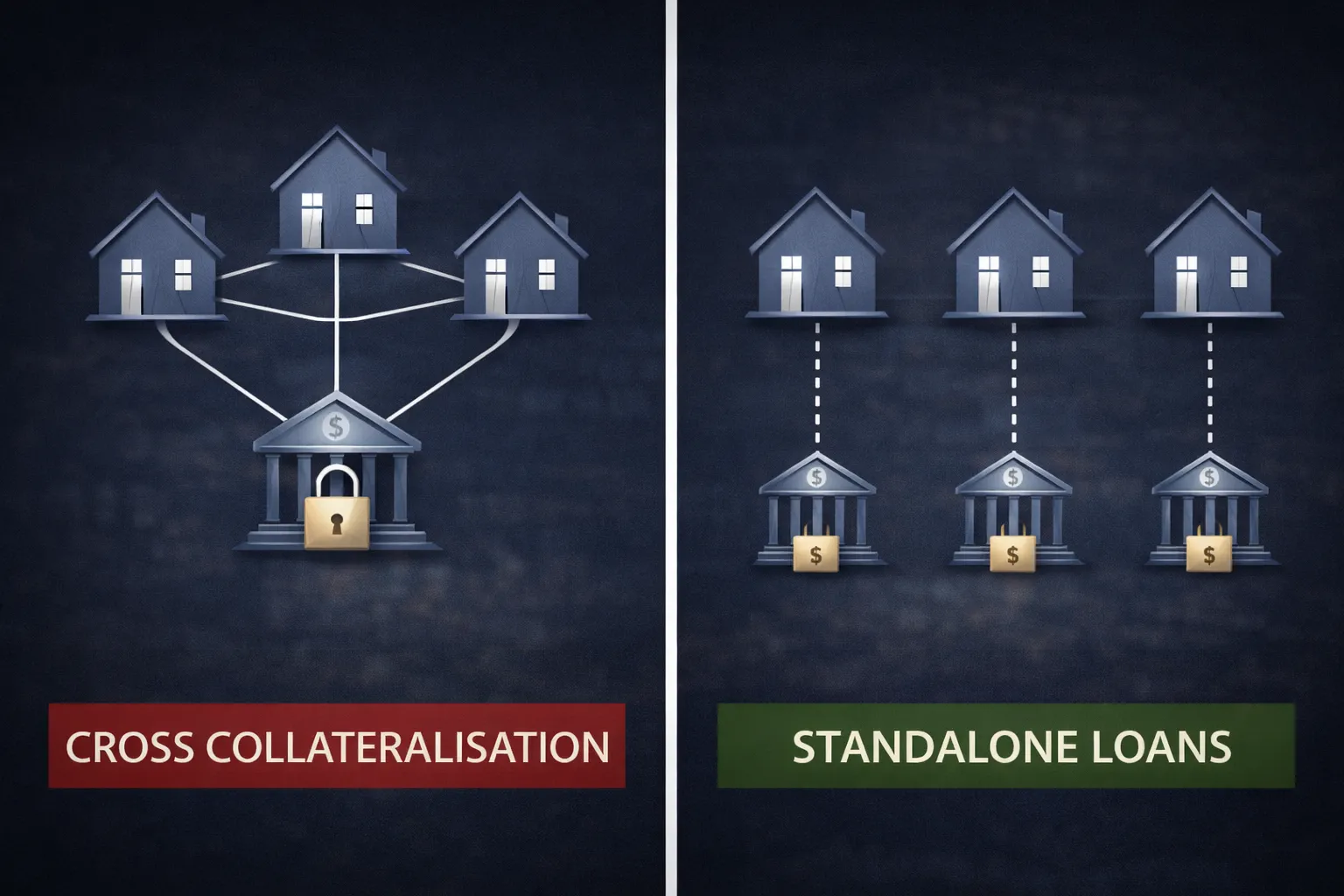

Strategy 3: Keep Your Loans Separate.

The key to scalable growth is to secure a standalone loan for each property. This keeps you in full control when refinancing your home loan or investments.

Strategy 4: Conduct an Annual Loan Review.

An annual checkup comparing fixed and variable interest rates ensures your loans are competitive and reveals equity for your next purchase.

Strategy 1: Get Preapproved for a Mortgage to Find Your Real Budget

The first step in any professional acquisition is to understand how to get preapproved for a mortgage. This crucial part of the application process involves submitting your financial documents to a lender for a formal assessment of your borrowing capacity.

This step is vital for understanding your true financial position before you begin your search. It also helps you learn how to increase borrowing capacity for the best assets and a larger loan amount.

The Mechanism The Serviceability Buffer

This is a strict safety rule used by all banks. Even if a home loan has a 6% interest rate, the credit team assesses your ability to meet repayments as if the rate were 9%. This 3% buffer is designed to ensure you can handle future interest rate rises.

If your finances can’t comfortably manage repayments at the higher test rate, the application will be declined. This assessment is a core part of managing debt and ensuring long-term financial stability.

The Anxiety It Solves: "Am I wasting my time?"

Online calculators often don’t apply this serviceability buffer, resulting in an inflated borrowing capacity. This creates false hope and leads investors to waste months searching for a property they can’t actually afford.

A formal preapproval provides a concrete, reliable figure that accounts for key factors affecting your borrowing capacity, such as your income and expenses. This gives you the confidence to search for the right property, so you can kick goals on your investment journey.

Strategy 2: Know the Right Property Price to Avoid Lender's Mortgage Insurance Surprises

Knowing a property’s true market value before making an offer is a critical risk management step. The standard industry mechanism is to engage a Certified Practising Valuer, who is an independent expert who calculates a property’s market value. The Australian Property Institute provides a directory to help you find a professional, unbiased assessment.

The Valuation Report

The valuer produces a detailed report based on objective data. This includes direct comparisons to recent, verified sales of similar properties, analysis of land value, and calculation of the building’s replacement cost.

This isn’t just an opinion: it’s an evidence-based financial assessment that helps explain the Loan-to-Value Ratio, especially in a competitive market where valuation shortfalls are a real risk.

What is Lender's Mortgage Insurance?

A common anxiety for home buyers is the extra cost of Lender’s Mortgage Insurance. This is an insurance premium the bank charges when your Loan-to-Value Ratio is above 80%, meaning your deposit is less than 20%.

A valuation shortfall occurs when you offer $1,000,000, but the bank’s valuation comes in at only $950,000. This can unexpectedly push your Loan to Value Ratio above 80% and force you to pay thousands in Lender’s Mortgage Insurance. An upfront valuation eliminates this risk.

Is Your Loan Structure Built for Growth?

The strategies in this playbook are powerful, but implementing them correctly is crucial. Our dual expertise as Buyer’s Agents and Certified Valuers ensures your finance structure is optimised for your next purchase and beyond.

Strategy 3: Keep Each Investment Loan Separate

To build a portfolio of multiple properties, the structure of your investment loans is more important than the interest rate. The default structure offered by many banks is often a trap for investors.

The Mechanism Of Cross Collateralisation

This is the technical term for when a bank links all your properties into a single loan facility. It uses your family home as security for your investment property loan and vice versa. While simpler for the bank, it removes your control.

The risks of cross collateralisation include trapping equity and limiting your ability to sell or refinance individual assets without impacting your entire portfolio.

The Anxiety It Solves: "Is my family home at risk? Will the bank trap me?"

The professional standard is to insist on a separate, standalone loan for each asset. Our buyer’s agent services always advise clients to use this structure as it isolates each property and keeps the owner in full control of their own capital.

It also greatly simplifies refinancing your primary home loan without affecting your investment properties. This is the single most important mechanism for safely scaling a portfolio.

Strategy 4: Annually Review Your Loans to Get the Best Deal

A successful portfolio is actively managed and not left on autopilot. An annual financial review with your mortgage broker is the mechanism to ensure your loans remain efficient and ready for growth.

The Annual Loan Review

In my experience, a structured annual meeting is the most effective approach. The agenda should be focused on three specific questions for your broker:

- “What interest rate would a new customer with my exact profile receive today?”

- “Based on current market values, what is my exact usable equity?”

- “Are any lenders offering more favourable investor policies right now?”

Comparing Fixed versus Variable Interest Rates

Your annual review is the ideal time to compare fixed and variable interest rates. By analysing Reserve Bank of Australia data, you can see historical trends and make an informed decision. If you find a better offer, refinancing can save you thousands and improve your cash flow for future investment opportunities. It’s smart banking to always look for the best deal.

Understanding Home Loan Options and Common Loan Terms

A fixed interest rate locks in your repayment amount for a set period, typically 1-5 years, which offers certainty. A variable interest rate moves with the market, meaning your repayments can change. For investors seeking predictable cash flow, a fixed-rate loan is often preferred. In contrast, those who believe rates might fall may choose a variable-rate loan.

Lender's Mortgage Insurance is a fee charged when you borrow more than 80% of a property's value. To avoid it, you must have a deposit of at least 20% of the purchase price. For example, on a $700,000 property, a $140,000 deposit would typically allow you to avoid this additional cost. Some government schemes can also provide assistance.

A Loan-to-Value Ratio is a percentage showing how much of a property's value you're borrowing. It's calculated by dividing the loan amount by the property's appraised value. For instance, if you're borrowing $400,000 for a property valued at $500,000, your Loan to Value Ratio is 80%. A lower ratio is seen as less risky by banks.

For those seeking stable growth and simplicity

- Residential Property is often the preferred choice. It's generally easier to secure loans for, simpler to understand for beginners, and benefits from more consistent capital growth driven by population demand. However, it typically offers a lower rental return and shorter lease terms.

For those seeking higher income and longer-term occupants

- A commercial property agent can be a strong option. It usually provides higher rental yields and longer leases, often 3-5+ years, with occupants frequently responsible for outgoings like rates and maintenance. The main tradeoffs're a higher sensitivity to economic downturns, longer potential vacancy periods, and the need for larger initial capital.

Yes, refinancing can be a powerful strategy. The primary goal is often to access the usable equity that's built up in a property. This equity can then be used as a deposit to purchase another investment. However, the tradeoff involves potential refinancing costs, so it's best suited for investors with a clear plan to expand their portfolio.

The difference between amateur and professional investors isn't luck: it's a commitment to a proven financial framework. Implementing these four strategies moves you from guesswork to a structured system designed to build wealth and protect your assets for the long term.

Ni Advocacy

Melbourne Buyers Agency

Build Your Portfolio with the Right Home Loan

Need help navigating the loan process? Let’s create your personalised home loan strategy together.