Key Takeaways: Pillars of a High-Performance Portfolio

Legal and Ownership Models

The most critical decision is choosing the right ownership. Setting up a trust, such as a Discretionary Family Trust, provides the highest level of protection by legally separating your investments from your personal holdings. This is a fundamental aspect of creating tax-efficient structures.

Finance Strategy and Gearing

Your loan setup dictates your risk and growth potential. This involves keeping home and investment loans separate to prevent cross-collateralisation and using an interest-only loan, a key component in many tax-aware strategies, to maximise cash flow for your next acquisition.

Tax Optimisation and Depreciation

A significant portion of your return comes from tax efficiency. This guide explains why ordering a report from a Quantity Surveyor is a non-negotiable step to claim a deduction for the building's wear and tear and lower your overall tax burden, including any future capital gain.

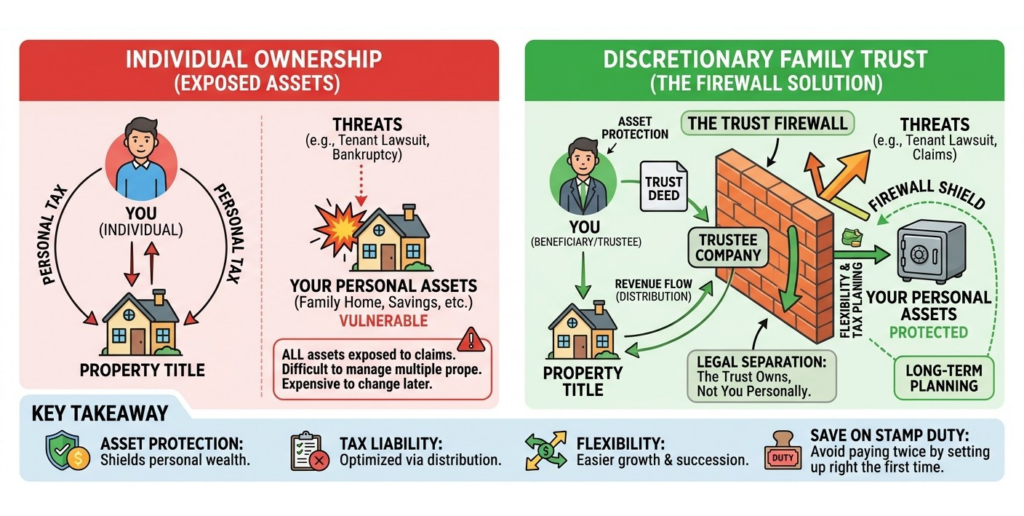

Pillar 1: Choosing Your Ownership Structure

The legal name listed on a title deed determines your tax liability, your legal exposure, and your flexibility to grow. The ownership model, whether a trust or a company, must serve your long-term goals. While some investors consider using their super, the rules for self-managed superannuation are complex and require specialist advice from a property investment advisor.

For most, the strongest option for asset protection is a Discretionary Family Trust. The process involves creating a legal entity where a trustee holds the property on behalf of beneficiaries (your family). With this trust ownership, the entity owns the real estate, not you personally.

Why this is a critical mechanic: This legal separation creates a firewall. If a tenant were to sue you, they’re suing the entity. Your personal holdings, including your family home, are shielded from the claim. Getting this company structure right is critical because it isn’t just about today but about safeguarding your future.

Our team collaborates directly with specialist accountants and solicitors to map out the optimal investment strategy for a client’s long-term goals before the search even begins.

The alternative of individual ownership leaves your personal assets exposed. Trying to move a property into this type of legal arrangement later means you must pay full stamp duty a second time on the current market value. It’s an extremely expensive mistake to correct, and one that proper planning avoids entirely.

Pillar 2: Finance Strategy for Safety and Growth

With your assets legally protected, you must structure your finances to be both safe and efficient for growth. Let’s get your finances kicking goals. This involves two non-negotiable rules for your property loan.

-

Financial Rule 1: Keep Your Lenders Separate

A critical error many investors make is allowing a bank to "cross-collateralise" their loans. This is a clause in the loan agreement that links your family home and investment real estate together as security for the bank.

The anxiety this solves: It prevents a scenario in which a problem with one loan could allow the bank to claim your family home. Using different, unlinked banks, for example, your home loan with ANZ and an investment loan with Macquarie, creates a financial firewall. This separation ensures your family's primary residence is completely isolated from the risks in your portfolio, offering superior security. -

Financial Rule 2: Use an Interest-Only Loan for Tax Benefits

The mechanical structure best suited for portfolio growth is a 5-year interest-only loan paired with a 100% offset account.

With negative gearing, your expenses exceed your rental income, creating a loss you can claim against your taxable income. An interest-only loan helps by keeping the loan balance high, which maximises the tax-deductible interest component. This increases your cash flow, allowing you to save much faster toward the deposit on your next acquisition. The tax implications of this strategy can be highly favourable.

An offset account is a transaction account linked to your mortgage. The cash balance is subtracted from your loan balance before the bank calculates interest. It allows you to reduce your interest payments while keeping your savings fully accessible, unlike a redraw facility, which can sometimes restrict access to your capital.

Ready to Build a High-Performance Portfolio?

A clear plan is the first step to building a high-performance portfolio. This guide has shown you the importance of structure, so now let’s map out your path forward with a custom strategy.

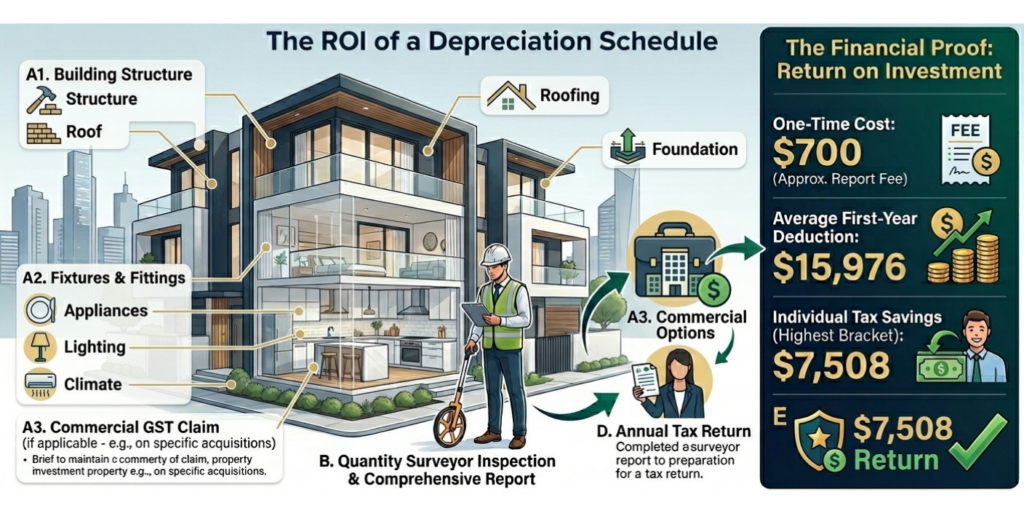

Pillar 3: Optimising Returns with a Depreciation Schedule

The moment you acquire an investment property, you must engage a Quantity Surveyor to prepare a depreciation schedule. The Australian Taxation Office (ATO) allows investors to claim a tax deduction for the decline in value of a building’s structure and its fittings over time.

This is also where GST can come into play for commercial acquisitions.

This is a fundamental component of managing your tax obligations effectively and a core part of any long-term portfolio review. The Quantity Surveyor inspects the property once and produces a report outlining all available claims.

Your accountant uses this report each year at tax time. This process is a non-negotiable part of a sound acquisition strategy, ensuring a client’s portfolio is built on a foundation of profit from day one.

These claims reduce your ordinary income, which is crucial for managing the property tax and eventual capital gain on a holding when you eventually divest. The financial return is significant. Based on data from BMT Tax Depreciation, a specialist in this field:

-

The Cost A one-time fee of approximately $700 for the report.

-

Average First-Year Deduction Investors can claim an average of $15,976.

-

Your Tax Savings For an individual in the highest tax bracket, this equates to $7,508 in tax returned.

Failing to get this report means you’re voluntarily overpaying the ATO. This isn’t just an oversight; it’s leaving money on the table. We prefer soaring above targets rather than leaving cash behind. By integrating these three pillars, you can operate a professional, high-performance investment portfolio.

Common Questions on Ownership and Tax Implications

For most investors seeking asset protection, a Discretionary Family Trust is a superior legal structure. It legally separates the investment from your personal holdings, shielding your family home from any potential litigation. One disadvantage compared to individual property ownership is a different land tax threshold in some states, but long-term security is a significant advantage. In certain situations, a company can also be used, though a trust often offers greater flexibility.

Negative gearing is a tax strategy where the deductible expenses of owning a rental property, primarily loan interest, exceed the rental income it generates. This creates a net rental loss. Under Australian tax law, you can deduct this loss from your other taxable income (like your salary), which reduces your overall tax liability for the financial year. This strategy is often used for new properties with higher depreciation benefits and interest costs.

A property depreciation schedule is a report by a specialist Quantity Surveyor that details the tax claims available for a building's wear and tear. It identifies the value of the structure (Capital Works) and its fittings (Plant and Equipment), calculating the decline in value you can claim each year. It's essential because it unlocks thousands of dollars in non-cash tax deductions, which lowers your taxable income without affecting your cash flow.

You'll legally reduce your Capital Gains Tax (CGT) liability using several established strategies. Key methods include holding the property for more than 12 months to qualify for the 50% CGT discount, using a trust to distribute the gain to beneficiaries in lower tax brackets, maximising your cost base by including all eligible costs, and timing the divestment for a financial year when your personal income is lower.

Using a Self-Managed Super Fund (SMSF) to buy property can be a powerful wealth creation strategy, but it's highly regulated and complex. The SMSF property investment rules are strict, involving a 'sole purpose test' and limitations on who can use the real estate. This strategy isn't suitable for everyone and requires specialist financial advice to ensure compliance and to determine if it aligns with your retirement goals.

Ni Advocacy

Melbourne Buyers Agency

Ready to Execute Your Playbook and Secure Your Future?

Let’s build the custom property strategy that protects your assets and accelerates your growth.