Key Takeaways On This Valuer's Framework for Choosing a Property

The core of the framework involves three actions

matching the asset (for example, houses and units) to your goal (growth and cash flow), analysing its financial health, and hunting for value.

Prioritise established properties

to avoid the 10-15% "new build premium": a marketing cost that can instantly erase your capital when buying a new build versus an established home.

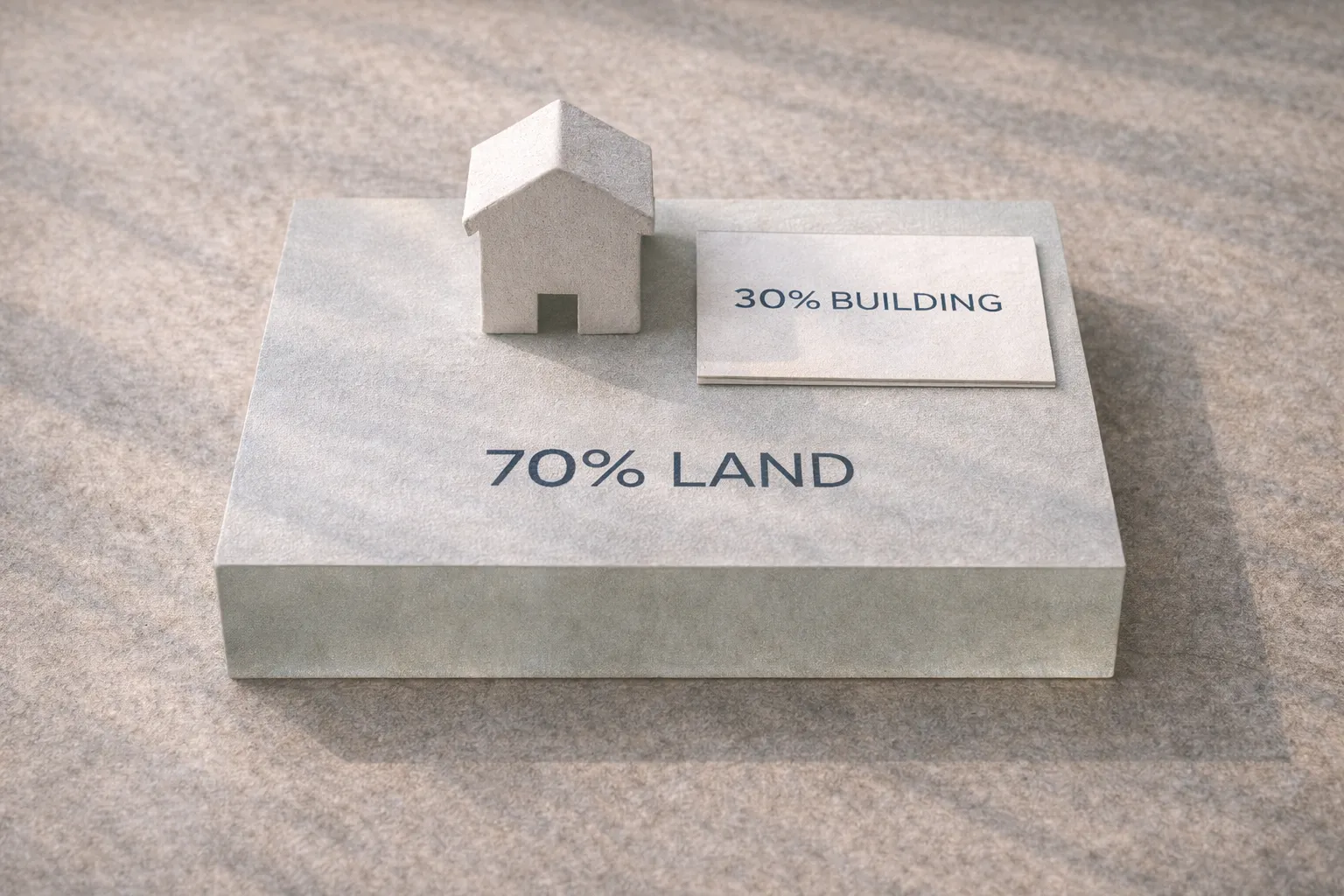

A high land-to-asset ratio is critical

because the ground itself appreciates while the building on it depreciates over time.

The best opportunities are often found

by targeting "stale" listings, researching future infrastructure zones, and accessing off-market assets through professional networks.

Comparing Different Types of Houses and Properties

A professional investment analysis relies on financial metrics, not guesswork. This matrix is the first and most important tool in the framework when considering different asset types. It shows you how to assess opportunities with the fact-based logic of a valuer, removing emotion from the decision-making process.

Metric

Primary Goal

Houses

Long-term capital growth.

Townhouses

A mix of long-term growth and rental income.

Apartments/Units

Immediate rental income (yield).

Metric

Key Metric to Check

Houses

Land to Asset Ratio (>60%). Land value appreciates while buildings depreciate. This is the engine of your wealth.

Townhouses

Scarcity. Look for small blocks (under 10) with unique layouts in good suburbs. Scarcity drives value.

Apartments/Units

Gross Rental Yield (>5.5%). The rental return must be high enough to compensate for slower value growth.

Metric

Biggest Financial Risk

Houses

Low Rental Income. A house might not earn enough rent to cover its costs, potentially requiring you to use your own funds to hold the asset.

Townhouses

Poor Strata Management. A badly run body corporate can lead to surprise costs and legal issues.

Apartments/Units

Oversupply. While vacancy rates remain low, high-density apartments can face oversupply risks, capping growth.

The Mechanics of Checking a Property’s Financial Health

Two key numbers reveal if a property’s a sound investment. Here are the steps to find them and what they mean for your strategy.

Calculate the Land to Asset Ratio

This is the percentage of the property’s total value held in the land itself.

- The mechanics: Ask the real estate agent for the latest council rates notice. Find the “Site Value” or “Land Value” and divide that number by the purchase price. A $600,000 site value on a $1,000,000 property yields a 60% land-to-asset ratio.

- Why it matters: The unspoken fear for every investor is buying an asset that doesn’t grow. The land appreciates due to scarcity, while the building on it loses value over time. A high ratio means more of your money’s in the growth component.

Calculate the Gross Rental Yield

This measures a property’s income potential before expenses are deducted. Understanding rental income and deductions is crucial, and the ATO provides a comprehensive guide for property investors.

- The mechanics: Multiply the weekly rent by 52 to get the annual income, then divide that by the purchase price. A property renting for $600 per week ($31,200/year) at a price of $650,000 has a Gross Rental Yield of 4.8%.

- Why it matters: This number indicates the property’s cash-flow efficiency. While state-wide yields average around 3.6%, a low yield on a specific apartment (for example, under 4%) is a red flag that you’re likely overpaying.

Other Residential Investment Options to Consider

Beyond common property types, some investors consider dual-occupancy homes or student accommodation. It’s also vital to understand ownership structures and local zoning, which you can explore through resources such as the Victorian Planning Schemes portal. Others may also look to buy vacant land for future development. Dual-occupancy properties offer two rental incomes but often have lower capital growth potential than traditional houses.

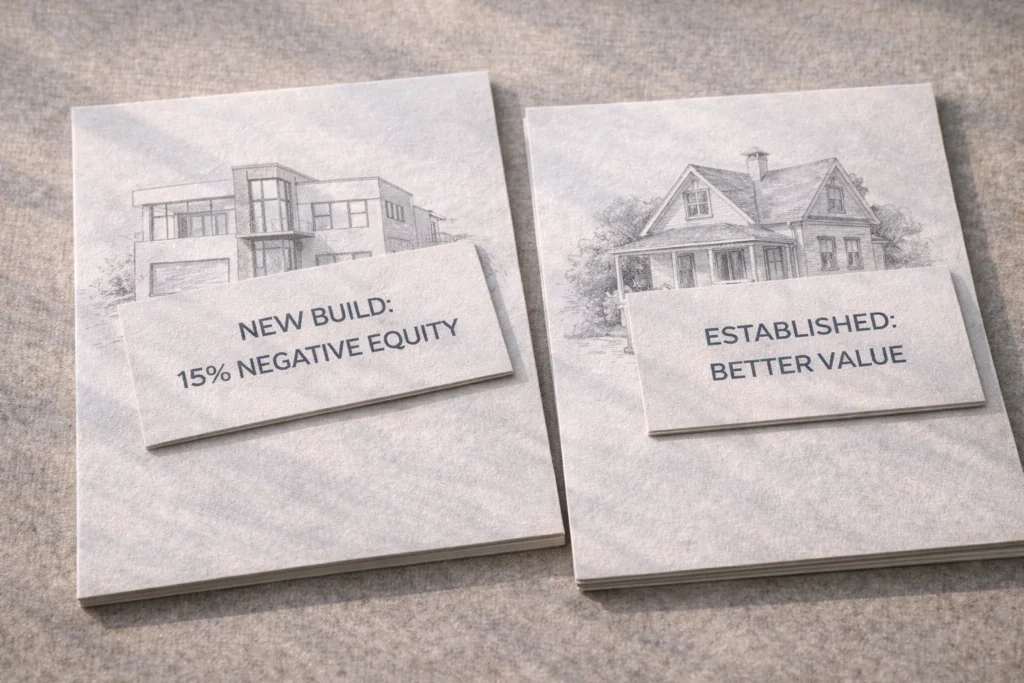

Buying a New Build vs. an Established Property: The New Build Trap

Choosing between a new and established home is a fundamental risk assessment. A “new build premium” is a common trap where the price is inflated by 10-15% to cover the developer’s profit and marketing costs.

How to Check for an Inflated Price

- The mechanics: On Realestate.com.au, find three established properties of a similar size in the same suburb that’ve recently sold. Calculate their price per square metre. If the new build’s 10-15% higher, that difference’s the premium you’re paying. This is the fact-based logic a Certified Property Valuer uses to determine a property’s true worth.

- The consequence: Without this check, you risk starting your investment journey with instant negative equity, meaning the property is worth less than you paid the moment you get the keys.

Find Your Ideal Investment Property

Let our team do the hard work. We find high-growth, off-market properties so you can invest with complete confidence and clarity.

3 Strategies to Find Properties Others Miss

The best investment-grade properties are rarely on the front page of real estate websites. A key part of successful property investment is knowing how to find an A-grade asset. Here are three executable strategies for finding better opportunities.

Strategy 1: Find Stale Listings

How to do it: On major property portals, search your target suburb and filter the results to show the 'Oldest Listings First'.

Why it works: After 60-90 days, sellers often become more anxious and willing to negotiate below their initial asking price, giving you leverage.

Strategy 2: Scan Government Infrastructure Maps

How to do it: Visit the official Victoria’s Big Build website and explore the interactive project map to see which suburbs are impacted by new transport links.

Why it works: Large-scale public infrastructure improves liveability and can boost local property values by 10-15%. This's how you buy in the path of predictable growth.

Strategy 3: Access Off-Market Properties

How to do it: Call the top-performing agents in your target suburb and ask to be added to their database for off-market or pre-market opportunities.

Why it works: A quiet sale saves agents' marketing costs and gives you access to properties before the general public.

For a personalised list of off-market properties that match this framework, you can book a complimentary, no-obligation strategy call with our team.

Your Final 3-Step Investment Blueprint

Before making an offer, run the potential investment through this final checklist. This ensures it’s a sound financial move and covers the crucial due diligence stage of the transaction. A clear property investment strategy is essential for success.

Define Your Goal, Then Match the Asset

Decide if your primary goal is long-term growth or immediate income. For growth, focus on houses with a high land-to-asset ratio (>50%). For cash flow, analyse established apartments for their rental yield (>4.5%).

Complete Due Diligence to Avoid Risk

To avoid buying a "lemon," engage a solicitor to review the contract and an inspector for a building report. This removes guesswork and provides a repeatable system for success. Our team rigorously applies this data-first framework to every potential acquisition, ensuring clients only see assets that are financially sound and primed for growth.

Hunt for Value Where Others Aren’t Looking

Dedicate at least 20% of your search time to the value-hunting strategies listed above. This's how you find the deals the average buyer'll never see.

Navigating the steps from an accepted offer to settlement and tenancy can be complex. Working with a professional property investment advisor streamlines this entire process, ensuring a smooth and successful acquisition.

Frequently Asked Questions

For long-term capital growth, a house is typically better due to its significant land component. In contrast, an apartment's superior for immediate rental income but generally slower growth and involves ongoing strata fees. The choice depends entirely on your financial goals.

The single biggest financial risk is the "new build premium": an inflated cost of 10-15% covering the developer's marketing and profit. This means your property is worth less than you paid for it from day one.

Two metrics are essential. First, the Land-to-Asset Ratio ensures value in the land's appreciation. Second, the Gross Rental Yield measures income-generating efficiency. A property with a high land component and a solid rental yield is a balanced and financially sound investment.

Yes, townhouses would be a good hybrid strategy. They typically offer better capital growth than apartments because they have more land and generate a stronger rental return than houses. However, focus on boutique blocks with a scarcity factor to maximise their value.

A great buyer’s agent combines market access with expert negotiation to secure the right property at the best price while saving you time and stress.

Ni Advocacy

Melbourne Buyers Agency

Ready to put this blueprint into action?

A Certified Valuer will build your personal acquisition plan to ensure your financial success.